The definitive solution to keep control of your e-notifications in Spain

PlatformVAT notifications is a webapp supported by the Spanish VAT specialist IVA Consulta, which aim is to provide non resident companies with an on-line tool to manage the reception and follow-up of the e-notifications received from the Spanish tax authorities.

Use our online solution to avoid

Incurring penalties

Losing Spanish VAT refunds

Missing claims

Reasons to use PlatformVAT Notifications

Do not risk missing your e-notifications in Spain and resulting dead-lines

Adopt any necessary actions

as may be required by the authorities

Be informed of any new e-notification you receive and control dead-lines

Outsource the managing of your Spanish e-notifications

Keeping track and managing the incidences related to the e-notifications in Spain received from the tax authorities in Spain is not always easy in case of non-resident companies (lack of the required e-signature certificate, language issues, risk of missing dead-lines, etc).

Outsourcing these tasks through the use of PlatformVAT notifications can be an easy solution in case of:

Non resident companies which due to their operative have registered in Spain and, as a result, are obliged to receive e-notifications from the Spanish authorities.

Internal tax departments and service centres of multinational groups which centralize the compliance with the tax obligations as regards group companies registered in Spain.

Tax advisors in other countries providing global tax advice to clients which scope includes Spanish tax compliance.

Discover the main features

|

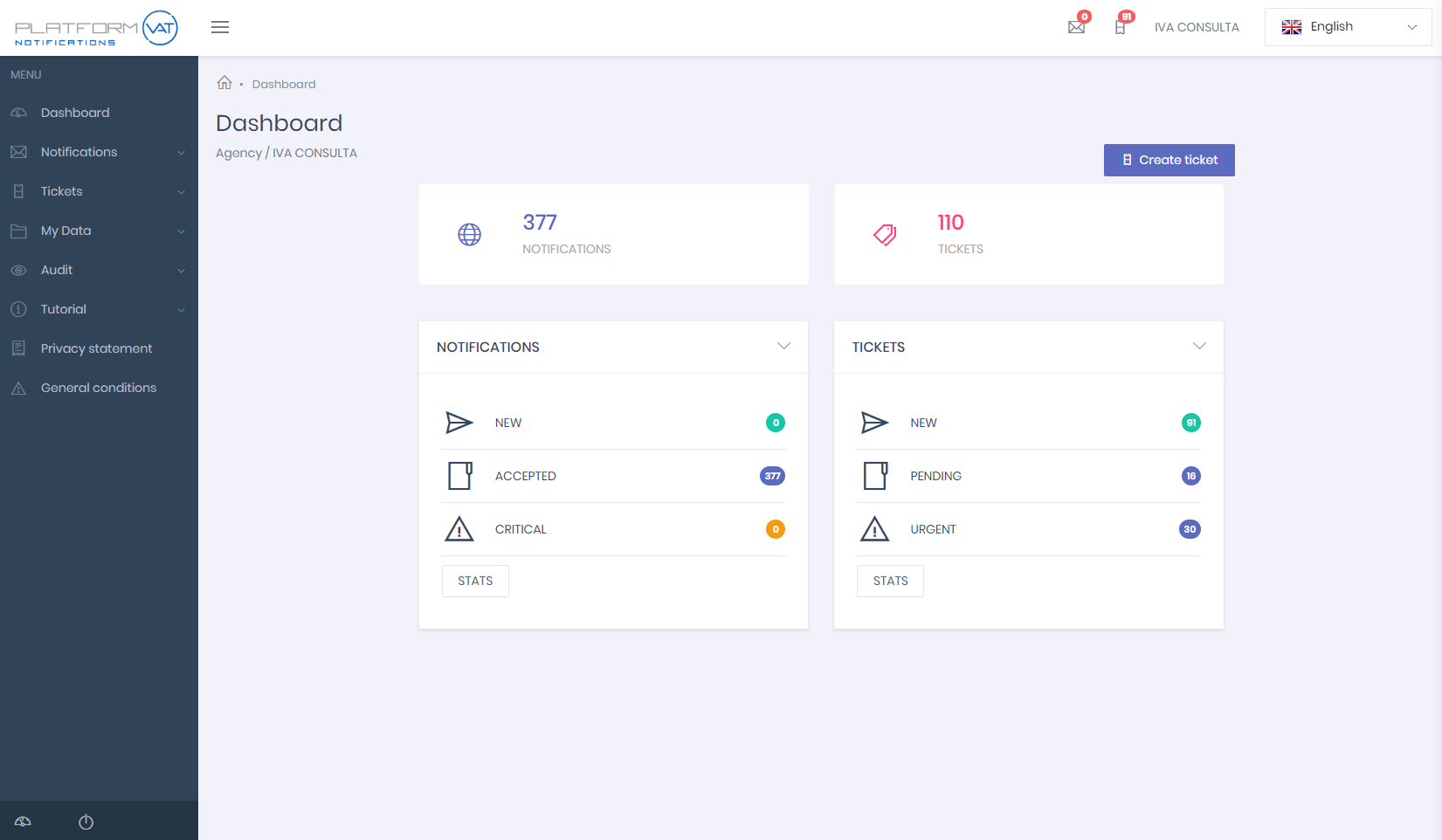

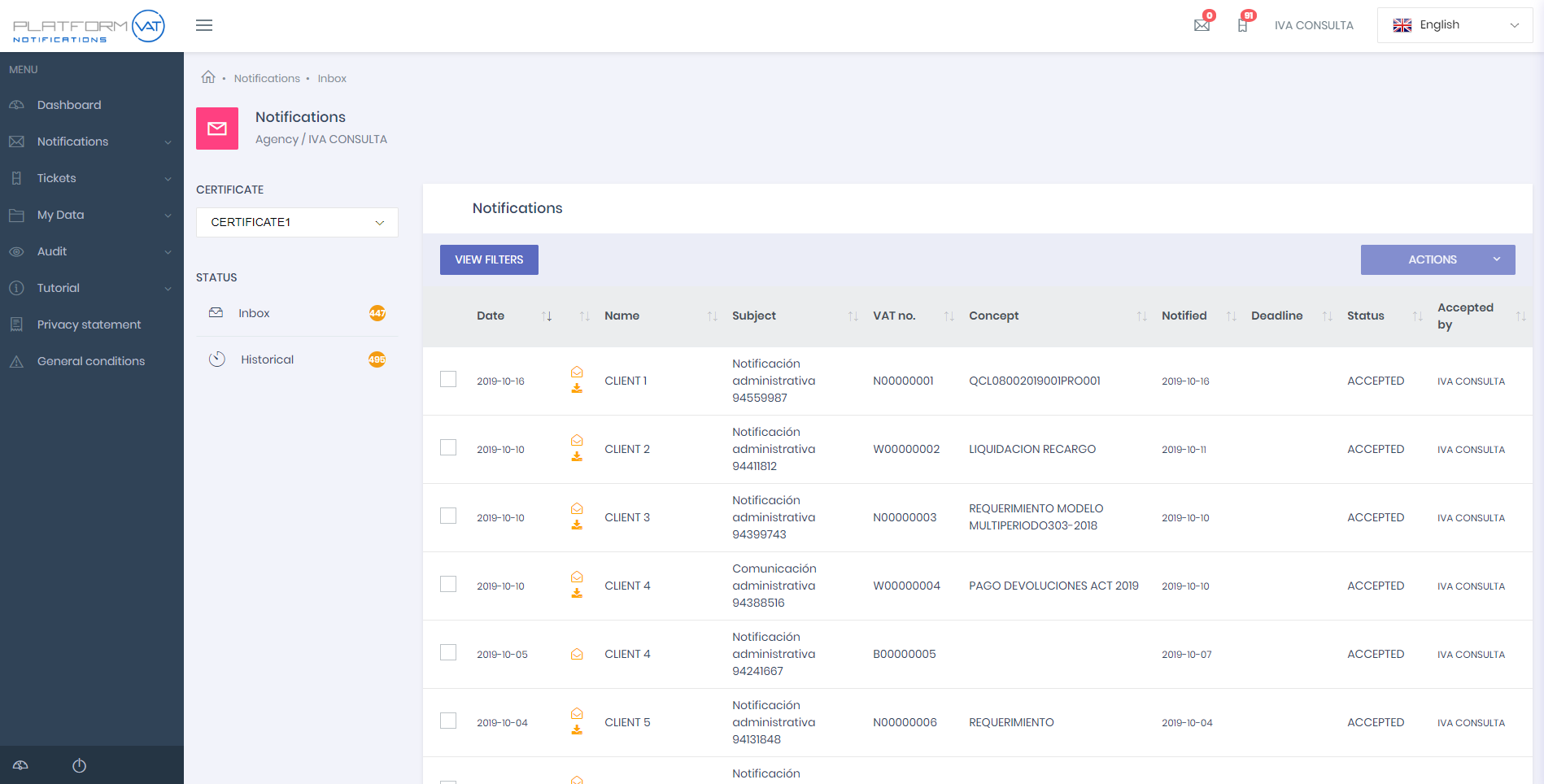

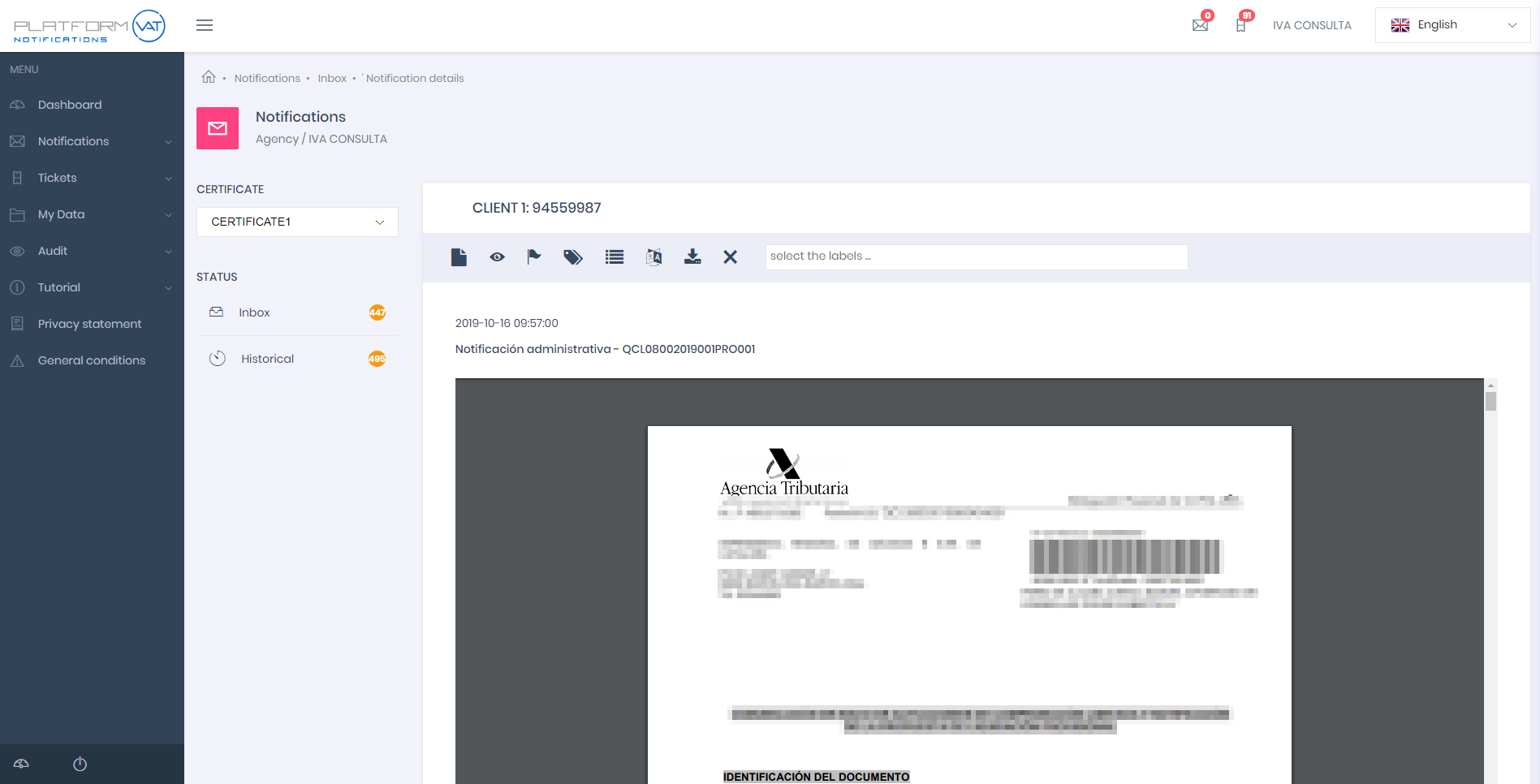

Control your new and outstanding e-notifications in Spain and tickets. Have a statistical overview of your on-going issues. |

|---|

|

Accept your new e-notifications in Spain. Manage your deadlines and take action. Check your e-notifications repository. |

|---|

|

Manage your e-notifications incidences by creating tickets for internal actions of external advice. Set-up dead-lines and warnings. Keep track of outstanding issues. |

|---|

About us

IVA Consulta is an office dedicated to consulting in the field of indirect taxation

The firm

IVA Consulta provides specialized VAT advice since 1.999 under the direction of Manuel Pérez de Algaba Cuenca, a Spanish lawyer with a long experience as tax advisor, including seventeen years in multinational firms.

After the introduction of the “Immediate Information Supply” system (SII) it offers an outsourcing service of the SII obligations. IVA Consulta has entered into strategic agreements with leading companies in the provision of VAT automation and global VAT compliance services.

It has also developed PlatformVAT, an on-line application of collaborative work for the provision of global VAT services and PlatformVAT Notifications a web app for the follow up of the electronic notifications from the Spanish Tax Management Agency (AEAT).

IVA Consulta forms part of the European VAT network International VAT Association (IVA) and of Tax, Tourism & Law (TTL), a network of professionals that specialize in advising the tourism sector.

Our team

Manuel Pérez de Algaba Cuenca, lawyer and economist. Managing partner of the firm. Founder member of VAT-Forum, a Belgian entity which engages in specialized training activities.

Pablo Luján Gil, lawyer. Partner of the firm. Advanced Master in European Law and International Taxation from the University of Maastricht. He has been a stagiaire in the TAXUD General Directorate of the European Commission in Brussels. Responsible for our “Global VAT Maintenance” service.

Eder Cruz Ubani, telecommunications engineer. During 2012 and 2013 he participates in the YUZZ program for entrepreneurs with innovative ideas based on technology, carried out by Banesto and selected for the INCUBE accelerator. Responsible for the implementation and maintenance of our tool PlatformVAT. Coordination with the internal IT managers of our clients.

Gloria Rodríguez de la Nuez, economist. Diplomate in Business Administration from the London Chamber of Commerce. Head of Administration and Finance.

Frequently Asked Questions

When a non resident company operating in Spain is obliged to register?

Under certain circumstances non resident companies operating in Spain are obliged to register at a census of taxpayers and obtain an internal tax identification number (hereafter referred to as “NIF”). This is applicable if:

- The company carries out any transaction that is located in the Spanish VAT territory for VAT purposes;

- Spanish VAT is due (regardless of whether or not the transaction is an exempt supply); and

- The company is the appointed taxable subject (this would not be the case with the supplier of goods or services should the so-called reverse charge rule apply).

There are no specific simplification measures in order to avoid VAT registration. As a result, there is no minimum threshold for the obligation to register.

qRegistration at the census so to obtain the NIF is a very straightforward process and involves the filing of the registration form (form 036) along with the required documentation at the corresponding tax office of the “Agencia Estatal de Administración Tributaria” (AEAT). The website of this Agency provides detailed information about the Spanish tax system and also provides a so-called “virtual office” where most procedures can be electronically managed.

When there is the obligation to obtain a Spanish VAT number?

The internal tax identification number is not enough for the case that a company intends to carry out intra-Community transactions to or from Spain. For this case, a Spanish VAT identification number must be obtained. The same is formed by adding the prefix ES to the NIF of the company.

This number is automatically granted following registration in the “Register of Intra-Community Operators” (RICO).

The application for registration in the RICO can be made on the same registration form use to apply for the NIF. However, the registration will not be cleared until the company provides documentary evidence that it has carried-out one intra-Community transaction under its Spanish NIF (purchase invoice, transport document, invoice for the transport, etc).

Once the registration is accepted, the taxable person will appear in the VAT Information Exchange System (VIES) database as having a Spanish VAT number. Until then, the taxable person will not have a Spanish VAT number. Registration in the RICO will be granted retroactively as of the date of the first intra-Community transaction.

Registration process

Registration at the census so to obtain an internal tax identification number (NIF) requires the filing of the registration form (form 036) along with the required documentation. To this end, the following documents and information will be needed.

- A copy of the incorporation deed and by laws (“Statutes”) of the company, as well as a recent certificate of the Register of Companies with the updated data, all duly stamped with the Hague Apostil along with a sworn translation of the same into Spanish.

- A power deed on behalf of a local mandatory so the same is empowered to file the registration form (model 036) in the name of the company. This power deed must be granted before a public notary of the country of residence and stamped with the Hague Apostil, unless you opt to get it legalized at a Spanish Consulate. At the power deed we will provide it is included a formal authorization on our behalf so we can access the electronic address of the company.

- A copy of the passport of the person signing the power deed on behalf of the company.

For the case that besides the NIF, the company applies for registration at the RICO so to obtain a Spanish VAT number, documentary evidence that it has carried-out one intra-Community transaction under its Spanish NIF will have to be provided, namely:

- Purchase invoice,

- Transport document,

- Invoice for the transport,

- Any other means of proof legally accepted (there is no numerus clausus).

How to contract the service?

The hiring of the services describe in this site is conditioned to the signing of the corresponding services agreement and the acceptance of the general conditions governing the provision of the same.

Obligation to receive e-notifications from the Spanish tax authorities in the official mail address

Royal Decree 1363/2010 of 29 October 2010 regulated electronic communications and notices by the State Tax Administration Agency (AEAT). This regulation, affecting almost all taxable persons since it applies to all commercial companies whether resident or not, introduced the obligation to receive most of the communications and notifications from the Spanish tax authorities by electronic means.

To this end, an official mail address (the so-called “dirección electrónica habilitada”) where such notifications are to take place, is automatically assigned by the tax authorities to any company obliged to register in Spain which is under the scope of the regulation. Prior to commencement of electronic notification to the company it must be informed of such circumstance by the Spanish Tax Administration.

The access to this official mail address will require the company to have an electronic signature certificate that is acknowledged by the tax administration. A third party with status of “social collaborator” and having such a certificate can be appointed to access the official mail address on its behalf.

Obtention of a valid electronic signature certificate so to access the official mail address

The company electronic signature certificate is to be issued to any individual holding legal representation wide enough for such a purpose. When this individual is not a Spanish resident the same must previously obtain a foreigner identification number (the so called NIE).

For this case, so to obtain the electronic signature certificate the following steps are required:

1.Obtention of the NIE of the legal representative.

- Printed-standard application (form EX-15), duly completed and signed by the new holder.

- Original and copy of the passport of the new holder.

- Power of Attorney granted on behalf of a local mandatory so to submit the NIE application at a police station in the Spanish territory. This document has to be notarized and duly stamped with the Hague Apostille.

This number can also be obtained at a Spanish consulate.

2.Obtention of the electronic certificate:

As mentioned, the holder of the electronic certificate of the company will be its legal representative. The following documents are required for its obtention:

- Power of attorney empowering the legal representative to obtain the certificate when the application is made at any Tax Office in the Spanish Territory. This document has to be notarized and duly stamped with the Hague Apostille.

- Official registration form (“legitimacion firma certificados RPJ”) completed and signed in each page by the company´s legal representative, where the signature is duly legalized (notarized and apostilled).

- An updated Certificate of the Register of Companies (dated no more than 15 days from the application date), with a sworn translation into Spanish, duly stamped with the Hague Apostille.

The application can be directly filed through certain Spanish consulates abroad.

The electronic certificate would have a 2-years validity, after which a new certificate must be obtained.

Empowering a third party to access the oficial mail address on behalf of the company

When a company obliged to receive e-notifications from the Spanish tax authorities lacks the required acknowledged electronic signature certificate to access its official mail address it is still possible to empower a third party to do so in its behalf.

This person or company must have the status of “social collaborator” according to the Spanish regulations (i.e. tax advisors, economists, lawyers, etc) and have such an acknowledged electronic signature certificate.

Except for the case in which the empowering is granted in person before the tax authorities, a special power deed will be required. The same will have to be granted before a public notary and stamped with the Hage apostil when issued abroad. This power deed must be produced before the Spanish tax authorities (AEAT) so the same is registered at a special register.

Do you need more information about how to manage your e-notifications of the Spanish VAT?

Do not hesitate to contact us